Quick summary:

- MiCA is the first EU-wide regulation dedicated to the crypto market.

- It applies primarily to crypto service providers and issuers of certain crypto-assets.

- Stablecoins are subject to a dedicated regulatory regime with stricter requirements.

- MiCA does not set crypto taxes and does not replace existing tax obligations in any EU member state.

- As an EU regulation, MiCA applies directly across all 27 member states — no separate national law required.

What is the MiCA Regulation?

Before MiCA, launching a crypto exchange in Europe meant dealing with 27 different regulatory frameworks. Germany wanted one thing, Estonia another, and several member states had no dedicated rules at all. Companies operated in a legal grey zone, and users had no real guarantee their funds were safe. The collapse of FTX in 2022 — when the platform used customer funds for its own bets and people lost billions — is the most cited example of what happens without clear rules.

According to the European Commission, MiCA aims to create a harmonised framework for the issuance of crypto-assets and the provision of related services across the European Union.

By introducing a single set of rules, the EU gives both users and businesses the clarity they need to operate with confidence across the single market.

What does MiCA stand for?

MiCA stands for Markets in Crypto-Assets Regulation.

The regulation works on a straightforward principle: depending on what type of company you are, you get a specific set of obligations. A stablecoin issuer must prove it holds the real reserves backing every token. A custodial exchange must keep customer funds separate and never use them for its own purposes. A broker must be transparent about costs and risks. Each type of activity, its own rules.

As an EU regulation — not a directive — MiCA applies directly in all 27 member states without requiring separate national implementing legislation. This creates a more predictable and uniform legal environment for everyone in the market.

EU documents frequently use the term “crypto-asset”, which is broader than “cryptocurrency” and covers cryptocurrencies, stablecoins, utility tokens, and other digital assets built on blockchain technology.

Why does MiCA matter?

The crypto market grew faster than regulation could keep up with. The result was users without real protection and companies operating in legal uncertainty.

MiCA addresses this by setting common standards across the entire EU. For users, that means more transparency and stronger protections. For companies, it means one authorisation that works across all 27 member states — no more navigating a different rulebook in every country.

When did MiCA come into force?

MiCA was published in the Official Journal of the European Union in 2023 and entered into force shortly after. Its provisions were rolled out in phases — stablecoin rules applied first, followed by the full framework for crypto-asset service providers.

| Event | Timeline |

|---|---|

| MiCA adopted | 2023 |

| Published in the Official Journal of the EU | 2023 |

| Stablecoin rules applied (ARTs and EMTs) | 30 June 2024 |

| Full CASP authorisation framework applied | 30 December 2024 |

| End of transitional period — all CASPs must be authorised | 1 July 2026 |

The technical standards and implementation timeline are developed and published by the European Securities and Markets Authority (ESMA), the institution responsible for coordinating MiCA’s application across EU financial markets.

Why was MiCA created?

The crypto market got too big to ignore — and the absence of clear rules had started costing users real money.

Over the past decade, crypto grew from a niche technology into a global industry with millions of users and assets worth hundreds of billions of euros. As adoption accelerated, European authorities concluded that a regulatory framework was needed to provide clarity and reduce risks for users and businesses alike.

A fragmented regulatory landscape

Before MiCA, crypto activity in Europe was regulated inconsistently — or not at all. Some member states had introduced their own rules; others had different approaches or no dedicated framework whatsoever.

In practice, this meant that an exchange authorised in Estonia might not meet any of the requirements Germany imposed. A user in the Netherlands relying on a platform registered in Malta had no clear idea which rules applied or what protections they had.

This created real obstacles for companies trying to scale across borders, and left users exposed to risks that varied dramatically depending on where their platform happened to be registered.

Protecting users

A key objective of MiCA is raising the level of protection for users across the EU.

Without clear rules, the crypto market saw platforms that gave users insufficient information, failed to separate customer funds from company funds, or lacked adequate risk management. The collapse of platforms like FTX and Celsius showed in the starkest possible terms what happens when these safeguards are missing — users lost access to their own funds overnight.

By introducing requirements around transparency and disclosure, MiCA gives users a higher baseline of protection — not eliminating investment risk, but ensuring they have the information they need to make informed decisions.

Building trust in the industry

Beyond user protection, MiCA is designed to support the sustainable growth of the crypto industry in Europe.

Clear rules make it easier for companies to enter the European market and for users to trust the services they use. A platform operating under MiCA authorisation has demonstrated to regulators that it meets minimum standards for governance, security, and customer protection.

At the same time, the regulation tries to strike a balance — creating guardrails without stifling the innovation that makes the crypto space dynamic.

What crypto-assets does MiCA cover?

MiCA doesn’t just regulate Bitcoin or Ethereum — it covers any type of digital asset that isn’t already regulated under existing EU financial law.

According to the EU framework, MiCA applies to crypto-assets and related services that fall outside other EU financial legislation. The regulation sets different rules depending on the characteristics of each asset type.

Bitcoin and other cryptocurrencies

The assets most users are familiar with — cryptocurrencies like Bitcoin, Ethereum, and Solana — fall within MiCA’s broader scope. These digital assets are widely used for investment, value transfer, and interacting with blockchain applications.

MiCA doesn’t regulate Bitcoin or Ethereum as assets in themselves — it doesn’t ban them, limit them, or control their price. What it does regulate are the companies offering services around them: the exchange where you buy them, the platform where you store them, the broker through which you trade them.

Stablecoins

One of the most closely regulated categories under MiCA is stablecoins — digital assets designed to maintain a stable value by reference to a fiat currency or other assets. Well-known examples include USDT and USDC, two of the most widely used stablecoins globally.

European regulators pay particular attention to stablecoins precisely because their stability makes them attractive for payments and transfers at scale. The more widely they’re used, the greater the potential impact of a collapse on the broader financial system. For this reason, MiCA requires stablecoin issuers to prove at all times that they hold the real reserves backing every token in circulation.

The classification of different crypto-asset categories and the requirements applicable to each are set out in Regulation (EU) 2023/1114 on markets in crypto-assets, published in the Official Journal of the European Union.

Utility tokens and other crypto-assets

MiCA also covers tokens used to access products, services, or blockchain ecosystems — commonly referred to as utility tokens.

Unlike cryptocurrencies such as Bitcoin, these tokens are primarily designed to unlock specific functionality within a platform. Well-known examples include BNB, BAT, and LINK.

Depending on the characteristics and purpose of each digital asset, the regulation may impose different requirements around issuance, documentation, and the provision of associated services.

Who does MiCA apply to?

If you buy, sell, or hold crypto for personal use, MiCA doesn’t require anything from you. The regulation targets companies, not individual users.

The bulk of MiCA’s obligations fall on companies that issue crypto-assets or provide services related to them. According to the European Commission, the regulation establishes common rules for issuers of certain crypto-assets and for crypto-asset service providers operating in the European Union.

Does MiCA apply to regular users?

People who buy, sell, or hold cryptocurrencies do not need to obtain a MiCA authorisation and have no licensing obligations under the regulation.

That said, you’ll feel the effects indirectly — through the platforms you use. If your exchange has to comply with MiCA, you’ll see clearer identity verification procedures, more detailed information about risks and costs, and the guarantee that your funds are kept separate from the company’s own money.

Which companies does MiCA apply to?

The regulation applies to a wide range of companies offering digital asset services in the European Union, including:

- cryptocurrency trading platforms;

- brokers and intermediaries;

- custody service providers;

- platforms facilitating the exchange between crypto-assets and fiat currencies;

- operators executing orders on behalf of clients;

- companies issuing certain categories of tokens and stablecoins.

Many of the services people use daily fall within MiCA’s scope in one form or another.

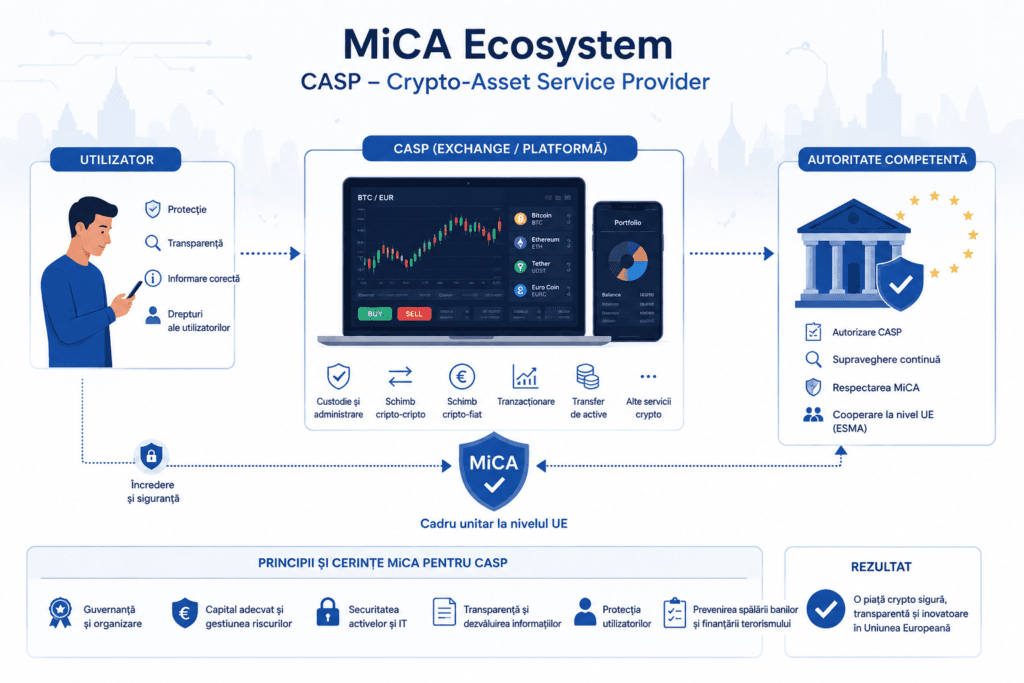

What is a CASP?

CASP stands for Crypto-Asset Service Provider — the official term in EU legislation for any company offering regulated services in the crypto space. If MiCA is the law, CASPs are the companies it applies to.

Binance, Coinbase, a local crypto broker, a custody platform — all of these are CASPs under MiCA, as long as they serve users in the EU.

Examples of CASPs

Depending on the services offered, a CASP might operate a trading platform, provide custody services, or facilitate exchanges between different types of digital assets.

Not every company in the blockchain industry is automatically a CASP. A blockchain software developer, for example, doesn’t become a CASP simply by working with the technology. What matters is whether the company is directly providing services to users involving their digital assets.

Why does the CASP concept matter?

Before MiCA, crypto service providers were subject to different rules depending on which member state they operated in. By introducing the CASP framework, MiCA creates a common standard for authorisation and supervision across the entire EU.

For you as a user, this means a CASP authorised in any EU member state can legally operate across the whole of Europe under the same standards. It doesn’t matter whether the platform is registered in Germany, the Netherlands, or Malta — the rules are the same.

This works through a “passporting” mechanism: once a company obtains MiCA authorisation from its home-state regulator — such as BaFin in Germany, the AMF in France, or the AFM in the Netherlands — it can passport its services to all other EU member states without needing separate authorisation in each country.

What services does MiCA regulate?

MiCA doesn’t just regulate which digital assets exist — it regulates what companies can do with them. In other words, it covers the services built around crypto-assets, not just the assets themselves.

According to Regulation (EU) 2023/1114 on markets in crypto-assets, activities that may fall under MiCA include the custody of crypto-assets, the operation of trading platforms, the exchange of crypto-assets for fiat currencies, and the execution of orders on behalf of clients.

Custody of crypto-assets

Custody means a company holds and manages your digital assets on your behalf. When you leave your Bitcoin on Binance or Coinbase instead of transferring it to your own wallet, you’re using a custody service.

It works similarly to a bank account: the bank holds your money and manages it on your behalf. In the same way, a crypto custody provider holds the private keys to your assets — without those keys, the assets cannot be accessed or transferred.

MiCA requires custody providers to keep client assets completely separate from the company’s own funds — the kind of safeguard that was absent at FTX, and whose absence is precisely why users lost everything when the platform collapsed.

Trading platforms

Trading platforms — exchanges — are probably the most familiar type of crypto service. They allow users to buy, sell, and trade crypto-assets through dedicated markets.

For example, a user can deposit euros, buy Bitcoin, later swap Bitcoin for Ethereum, and keep the assets on the platform until withdrawal. In most cases, the provider also holds and manages user assets, offering integrated accounts, wallets, and trading tools similar to those found on traditional financial markets.

Under MiCA, operators of these platforms must meet requirements around transparency, risk management, and user protection.

Exchange of crypto-assets for fiat currencies

This is the service you use when you buy Bitcoin with euros or sell Ethereum and receive money in your bank account. It works similarly to a currency exchange — except instead of dollars for euros, you’re swapping crypto for traditional money.

Although many exchanges offer both trading and crypto-to-fiat conversion, MiCA treats these as distinct services — each with its own compliance obligations.

Order execution and other associated services

The regulation also covers activities such as the execution of orders on behalf of clients, the reception and transmission of orders, and the provision of certain advisory services related to crypto-assets.

In plain terms: if a company acts on your behalf in the crypto market — placing orders, managing transactions, or offering investment recommendations — it falls under MiCA too.

What obligations do crypto service providers have?

Getting authorised is just the first step. Once authorised, a crypto service provider must follow a concrete set of rules — different depending on the type of service offered, but with several obligations that apply across the board.

Before MiCA, the requirements applicable to these companies varied significantly from one member state to another. MiCA aims to harmonise these rules and establish a minimum level of user protection across the entire EU.

Authorisation and ongoing supervision

The most fundamental obligation is this: without authorisation, a company cannot legally operate in the EU. Through this mechanism, national competent authorities verify that a company meets the necessary conditions before it can offer services to European users.

Obtaining authorisation requires meeting requirements around organisational structure, company governance, and operational risk management. In practice, crypto service providers must also implement compliance procedures including customer identity verification (KYC – Know Your Customer) and measures to prevent money laundering (AML – Anti-Money Laundering).

That’s why platforms ask for your ID and a selfie when you sign up — not because they want to, but because MiCA requires it.

Protection of client funds and assets

MiCA introduces clear obligations around protecting assets held on behalf of clients. Your funds and assets must be kept separate from the company’s own money — the company cannot use them for its own operations, investments, or expenses.

The purpose of these requirements is to reduce the risk of user assets being affected by operational problems, mismanagement, or conflicts of interest.

Transparency and user information

Companies must provide clear information about the services they offer, the associated costs, and the risks relevant to users — before the user engages with the service, not buried in terms and conditions nobody reads.

The goal is to ensure that people using crypto services can make better-informed decisions and understand what they’re actually signing up for.

Managing conflicts of interest

MiCA includes requirements around identifying and managing conflicts of interest that can arise in the operations of crypto service providers.

A concrete example: an exchange that lists its own tokens and simultaneously executes client orders on those same tokens has an obvious conflict of interest. MiCA requires companies to identify these situations, disclose them, and manage them in a way that doesn’t compromise user interests.

How does MiCA affect regular users?

Most of MiCA’s obligations fall on companies, not on you. But the way those companies comply with the rules has a direct impact on your experience as a user.

More transparency

Before you use a service or buy a crypto-asset, the platform is required to give you clear information about what you’re buying, what risks it involves, and what it costs. Not after, not buried in pages of terms and conditions — before.

In practice, you’ll notice more detailed documentation about the services offered, clear risk warnings about volatility, and terms of use that are actually readable.

Stronger user protection

MiCA introduces requirements around the management of client assets, complaint handling, and communication with users.

Concretely: if you have a problem with a MiCA-authorised platform, there are clear procedures through which you can file a complaint. And your assets are protected by the mandatory separation from company funds — if the platform goes bankrupt, your money doesn’t go with it.

The regulation doesn’t eliminate the risks associated with investing in digital assets, but it raises the bar for companies operating in the European Union.

Changes to verification procedures

As providers implement MiCA’s requirements, you may notice changes to registration and verification procedures. If a platform suddenly asks for more documents or requests re-verification of your identity, it’s most likely part of the process of aligning with the new European framework.

MiCA does not replace your tax obligations

It’s important to understand that MiCA and crypto taxation are two completely separate topics.

MiCA regulates companies and the crypto market. The taxes you owe on crypto gains are governed by the tax legislation of each member state — in Germany by the Bundeszentralamt für Steuern, in France by the Direction générale des Finances publiques (DGFiP), in the Netherlands by the Belastingdienst, and so on. MiCA doesn’t change what you owe to your national tax authority.

Users who generate income from crypto transactions must continue to determine and declare their tax obligations under the rules applicable in their country of tax residence.

Will MiCA make cryptocurrencies safer?

MiCA makes platforms safer — not cryptocurrencies themselves. Bitcoin will still be volatile. Ethereum can still drop 50% in a week. Solana can still have technical issues.

What changes is that the platform where you buy them must follow clear rules, protect your funds, and be transparent with you. The regulation doesn’t guarantee profits and doesn’t eliminate the risk of losing capital — but it works toward creating a more predictable and safer environment for users and service providers alike.

MiCA and stablecoins

Of all the crypto-asset categories covered by MiCA, stablecoins face the strictest regulatory regime. The reason is straightforward: they’re designed to be stable, which makes them attractive for payments at scale — and the more widely they’re used, the greater the potential impact of a collapse on the broader financial system.

Why does MiCA pay special attention to stablecoins?

Unlike assets such as Bitcoin or Ethereum, stablecoins are designed to maintain a stable value by reference to one or more assets. This makes them useful not just for investment, but for payments, international transfers, and interacting with financial applications built on blockchain.

The collapse of TerraUST in 2022 is the clearest example of what happens when a stablecoin doesn’t have the real reserves to back it up. In the space of a week, a token designed to always be worth one dollar went to zero — wiping over $40 billion from the market. This is exactly the scenario MiCA’s stablecoin rules are designed to prevent.

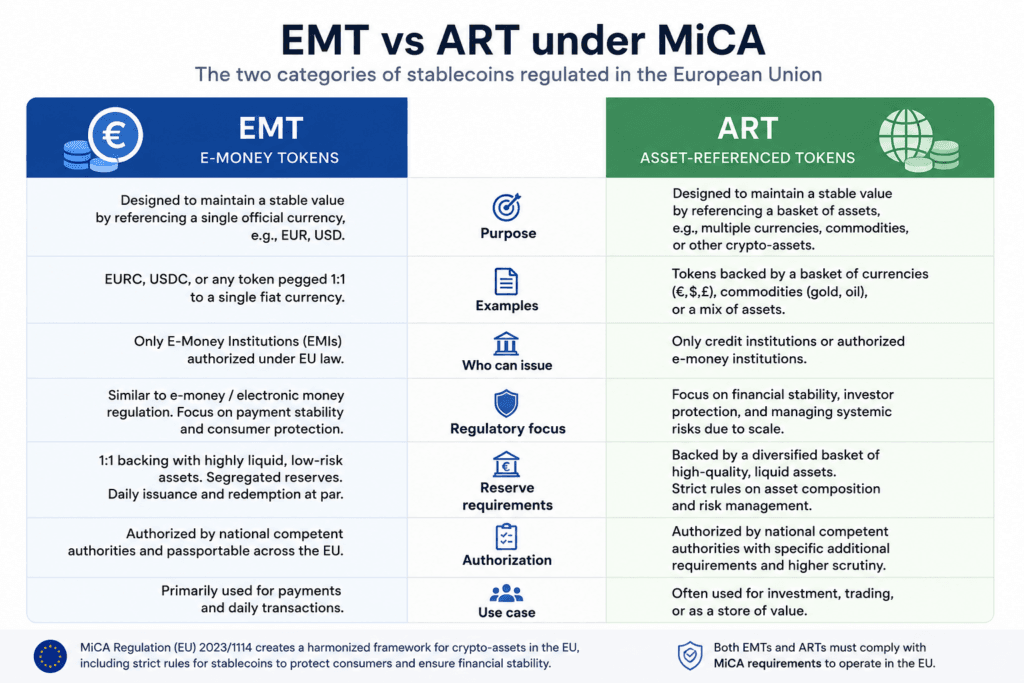

What are EMTs and ARTs?

MiCA divides stablecoins into two main categories, each with its own set of obligations.

An EMT (E-Money Token) is a stablecoin pegged to a single fiat currency — for example, a token always worth one euro or one dollar. USDC and EURC are typical examples. The issuer of an EMT must hold equivalent fiat reserves in separate bank accounts at all times. EMT issuers must also be authorised either as a credit institution or as an electronic money institution — MiCA layers its requirements on top of the existing Electronic Money Directive.

An ART (Asset-Referenced Token) is a stablecoin pegged to multiple reference assets simultaneously — this could be a basket of fiat currencies, commodities like gold, or other assets. Meta’s former Libra project was conceived as an ART. The obligations for ART issuers are even stricter, given that greater complexity means greater potential risk.

The distinction matters for issuers, not for users — but understanding it helps explain why MiCA treats a token like USDC differently from a more complex multi-asset stablecoin.

What do these rules mean for users?

For you as a user, the EMT and ART classification doesn’t change how you use stablecoins day to day. You’ll still send USDT, hold USDC, or make payments in digital euros exactly as before.

What changes behind the scenes: the issuer is required to permanently prove it holds the reserves backing the token, publish regular reports, and be supervised by authorities. The reserve composition rules under MiCA also limit how much can be held with any single bank — reducing the kind of concentration risk that destabilised USDC during the Silicon Valley Bank failure in March 2023.

The chance of a TerraUST-style collapse for a MiCA-regulated stablecoin becomes significantly lower.

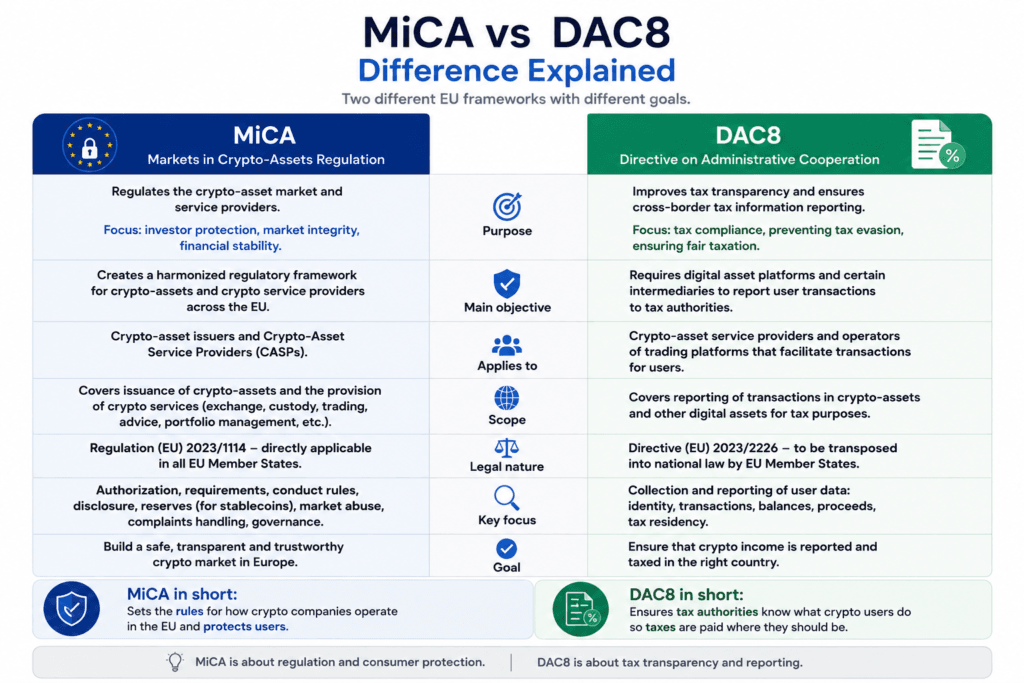

What is the difference between MiCA and DAC8?

MiCA and DAC8 are two separate European initiatives that are frequently confused — understandably so, since both emerged around the same time and both affect the crypto industry. But they serve completely different purposes.

MiCA regulates how the crypto market operates. DAC8 regulates how crypto transactions are reported to tax authorities.

To put it plainly: MiCA is for companies, DAC8 is for tax authorities. MiCA sets the rules for how the crypto market functions. DAC8 ensures that information about your transactions reaches the relevant tax authority in your country — whether that’s the Bundeszentralamt für Steuern in Germany, the DGFiP in France, the Belastingdienst in the Netherlands, or the equivalent authority wherever you’re tax resident in the EU.

| MiCA | DAC8 |

|---|---|

| Regulates the crypto market | Regulates tax reporting |

| Targets crypto service providers | Targets the transmission of information to authorities |

| Introduces rules for CASPs | Introduces reporting obligations |

| User protection and market stability | Tax transparency and automatic information exchange |

The European Commission confirms that DAC8 extends automatic information exchange to cover crypto-asset transactions and the relevant crypto service providers operating across EU member states.

MiCA and DAC8 don’t replace each other — they work together. MiCA requires exchanges to get authorised and follow clear rules. DAC8 requires those same exchanges to report user transaction data to tax authorities across member states. If you trade on a MiCA-authorised platform, your national tax authority will know — through DAC8 — what you’ve bought and sold.

The practical implication is clear: the argument that “the tax authority doesn’t know about my crypto transactions” is becoming less and less valid across the EU. DAC8 closes the information gap that previously allowed crypto gains to go unreported in many jurisdictions.

How does MiCA apply across the EU?

Because MiCA is an EU regulation — not a directive — it applies directly in all 27 member states without requiring separate national implementing legislation. Once it entered into force, it became binding law across the entire European Union simultaneously.

This means that crypto service providers operating anywhere in the EU must comply with the requirements set out in Regulation (EU) 2023/1114 for any activities that fall within MiCA’s scope.

In practice, however, implementation has not been perfectly uniform. Member states had discretion over certain transitional arrangements, and some moved faster than others.

How different countries have approached MiCA

Germany

Germany chose a shorter transition period than the EU maximum, cutting its national window to 31 December 2025. BaFin — the Federal Financial Supervisory Authority — authorised over 50 CASPs as of mid-2026, the highest number in the EU. This reflects Germany’s pre-existing licensed financial sector converting to MiCA rather than an easy entry path for new players. BaFin is widely considered the EU’s most demanding crypto regulator, and the high number of authorised firms stems largely from established financial institutions transitioning from prior licensing regimes rather than new market entrants.

France

France built its MiCA supervision on top of the existing PSAN regime (Prestataire de Services sur Actifs Numériques), introduced back in 2019. The AMF — Autorité des Marchés Financiers — offered a streamlined transition path for firms already registered under the previous French regime. France also leads the EU in EMT issuers, including Société Générale-FORGE with its EURCV stablecoin — an early signal of how traditional financial institutions can enter the regulated crypto space under MiCA.

The Netherlands

The Netherlands applies some of the strictest substance requirements in the EU. The AFM — Authority for the Financial Markets — requires a registered office in the Netherlands, genuine local staff, and real operational presence before an application even advances. Shell structures are identified and flagged at the intake stage, resulting in a smaller but more carefully vetted cohort of authorised firms.

Spain

Spain applied the full 18-month transitional period, with the CNMV — Comisión Nacional del Mercado de Valores — having begun accepting CASP applications in September 2024.

Italy

Italy shares oversight between CONSOB and Banca d’Italia, having transitioned from its legacy OAM registry to the MiCA framework.

The passporting advantage

One of MiCA’s most significant practical benefits is the single passport. Once a company obtains authorisation from its home-state regulator — BaFin, AMF, AFM, CNMV, or any other national competent authority — it can offer its services across all 27 EU member states without needing separate authorisation in each country.

This fundamentally changes the economics of operating in Europe. Before MiCA, scaling across borders meant navigating 27 different regulatory frameworks. Now it means one application, one authorisation, one passport.

One structural shift worth noting: the passporting mechanism has begun to consolidate where crypto companies choose to incorporate. Jurisdictions with efficient, well-resourced regulators — Germany, France, the Netherlands — are attracting more applications, while countries that haven’t yet fully implemented MiCA’s national framework face uncertainty for companies incorporated there.

What does this mean for you as a user?

If you use a MiCA-authorised platform — whether it’s registered in Germany, France, the Netherlands, or anywhere else in the EU — you benefit from the same protections. The rules are identical regardless of where the company is incorporated.

Concretely, you’ll notice:

- more rigorous identity verification at registration or periodically;

- clearer information about risks and costs before you use a service;

- the guarantee that your assets are kept separate from the platform’s funds;

- clear complaint procedures if something goes wrong.

For regular users, MiCA introduces no additional authorisation or licensing obligations. You buy, sell, and hold crypto exactly as before — just with stronger protections behind the scenes.

A practical example

Say you use an exchange registered in the Netherlands that serves clients across Europe. Before MiCA, that exchange operated under Dutch rules — which could be completely different from what France or Spain required. Now, regardless of where it’s registered, it must follow the same MiCA rulebook for all EU users.

Advantages and criticisms of MiCA

Like any major piece of legislation, MiCA has been received with both enthusiasm and reservations from participants in the crypto market. Supporters see it as a necessary step toward maturity for the industry. Critics argue that the compliance burden could stifle innovation — particularly for smaller players.

The case for MiCA

The most significant benefit is the single rulebook. Before MiCA, a company wanting to operate across Europe faced 27 different regulatory frameworks — separate legal costs, separate applications, separate compliance teams in each jurisdiction. Now one authorisation opens the entire EU market.

For users, the advantages are equally concrete. Platforms are required to keep client assets separate from company funds, be transparent about costs and risks, and handle complaints through structured procedures. The level of protection on a MiCA-authorised platform is meaningfully higher than what existed before.

A third benefit is the credibility effect. Clear regulation makes it easier for institutional investors, traditional financial firms, and more conservative users to engage with crypto. Several major banks across the EU have already begun exploring tokenisation and digital asset services precisely because MiCA provides the legal certainty they require.

France’s Société Générale-FORGE issuing a regulated euro stablecoin and the European Investment Bank issuing digital bonds on Ethereum are early signals of what institutional adoption looks like under a clear regulatory framework.

Criticisms and limitations

The most frequently heard criticism is that compliance costs are high — especially for smaller companies and early-stage projects. Obtaining MiCA authorisation requires legal, technical, and operational resources that startups rarely have. There’s a genuine risk that MiCA ends up favouring large, well-resourced players over smaller innovators, as Germany’s experience illustrates: BaFin’s authorised CASPs are predominantly conversions from the pre-existing licensed financial sector, not new entrants.

A second criticism targets the pace of technology versus the pace of legislation. Blockchain evolves quickly — DeFi, NFTs, new tokenisation models emerge constantly. MiCA was written for the reality of 2022-2023 and may become partially outdated as the technology evolves.

DeFi is the most obvious gap. Decentralised applications and protocols without a central operator don’t fit neatly into MiCA’s authorisation framework — if there’s no identifiable company to authorise, the regulation becomes difficult to enforce. European authorities acknowledge this limitation and it’s expected to be addressed in future iterations of the framework.

Finally, MiCA doesn’t eliminate investment risk. Even in a regulated environment, crypto-assets remain volatile and projects can fail. A MiCA authorisation is not a quality stamp on the asset itself — it’s a quality stamp on the service provider. Users still need to evaluate their own financial decisions carefully.

How has the crypto market changed since MiCA?

Before MiCA, the European crypto market operated as a patchwork of national regimes where rules differed dramatically from one country to the next. After MiCA, there is a single standard across the entire EU.

| Before MiCA | After MiCA |

|---|---|

| Different rules in each member state | Single legislative framework across the EU |

| Different requirements for crypto service providers | Harmonised rules for CASPs |

| Limited clarity on stablecoin regulation | Dedicated regime for EMTs and ARTs |

| Different standards for user protection | Common transparency and risk management requirements |

| Fragmented supervision across Europe | Coordination and standardisation at EU level |

In practice, the changes have been felt across the industry in several concrete ways.

The major platforms — Binance, Coinbase, Kraken — began MiCA authorisation processes and adapted their product offerings for European users. Some services available in other parts of the world have been restricted or modified for the EU market specifically to comply with MiCA requirements.

Some smaller exchanges that lacked the resources for compliance chose to exit the European market rather than invest in the authorisation process. The result is fewer players, but better regulated ones.

The 1 July 2026 deadline marked the end of the transitional period. After that date, no crypto-asset service provider may legally provide crypto-asset services in the European Union without MiCA authorisation. Companies that failed to obtain authorisation were required to cease operating or complete an orderly wind-down of their EU crypto-asset services.

For users across the EU, the most visible change has been at the level of identity verification procedures and platform documentation. More paperwork at registration — but also more protection once you’re a client.

Although the crypto market continues to evolve rapidly, MiCA represents one of the most significant attempts to create a common legislative framework for digital assets at a continental scale. The regulation is no longer only about preparation — it is now about enforcement, with every crypto business operating in or serving the EU expected to be fully aligned with its requirements.

What does MiCA not regulate?

MiCA is a comprehensive regulation, but it doesn’t cover everything. There are important areas of the crypto ecosystem where the regulation doesn’t apply — or applies only partially.

MiCA does not set crypto taxes

MiCA and crypto taxation are completely separate topics. The regulation sets the rules for companies and the market — it doesn’t determine how much tax you pay on your crypto gains.

Tax obligations are governed by the fiscal legislation of each member state. In Germany, gains from crypto disposals held for less than one year are taxed as income by the Bundeszentralamt für Steuern. In France, the DGFiP taxes crypto gains at a flat rate under the PFU (Prélèvement Forfaitaire Unique). In the Netherlands, the Belastingdienst applies a wealth tax model based on deemed returns. The rules differ significantly across the EU — MiCA changes none of them.

Regardless of whether the platform you use is MiCA-authorised, if you’ve made a profit from crypto, you have an obligation to declare it to your national tax authority.

MiCA does not eliminate investment risk

A regulatory framework doesn’t make crypto investments safe. Bitcoin can still drop 80% in a bear market. Ethereum can still lose half its value in a month. A project can still fail even if it’s listed on a fully MiCA-authorised platform.

MiCA works to increase transparency and raise standards at the platform level — it doesn’t guarantee returns and doesn’t eliminate the possibility of losing your capital.

MiCA does not ban cryptocurrencies

Despite some misinterpretations that have circulated publicly, MiCA does not ban or restrict users from holding or using cryptocurrencies. You can continue to buy, sell, and hold Bitcoin, Ethereum, or any other crypto-asset.

MiCA’s purpose is to regulate the companies and services in the industry — not to restrict individual users.

MiCA does not cover all crypto activities

There are activities that fall outside MiCA’s direct scope. If you hold your own digital assets through a self-custody wallet — Ledger, Trezor, Electrum — you don’t become a crypto service provider and have no obligations under MiCA.

Decentralised applications and DeFi protocols also remain a grey area. They operate without an identifiable central operator that can be authorised in the traditional sense. European authorities acknowledge this limitation, and it’s widely expected that future versions of the regulatory framework will address this segment of the market more directly.

Most non-fungible tokens (NFTs) are also outside MiCA’s scope — the regulation explicitly excludes unique and non-fungible crypto-assets, though the boundary can become unclear when NFTs are issued in large series or used in ways that resemble financial instruments.

MiCA does not replace DAC8

MiCA and DAC8 are two distinct European initiatives with different objectives. MiCA regulates how the crypto market functions. DAC8 focuses on tax transparency and the automatic exchange of information between tax authorities across member states. The two work together — they don’t replace each other.

Frequently asked questions about MiCA

Does MiCA ban cryptocurrencies?

No. MiCA does not ban cryptocurrencies or restrict users from holding or using them anywhere in the EU. MiCA targets the companies providing crypto services — not the individuals who buy or hold digital assets.

Is Bitcoin regulated by MiCA?

Bitcoin as an asset is not regulated by MiCA — nobody can control the Bitcoin protocol. What MiCA regulates are the services built around it: the exchange where you buy it, the platform where you store it, the broker through which you trade it. If those companies operate in the EU, they must comply with MiCA.

Does MiCA apply across all EU member states?

Yes. As an EU regulation, MiCA applies directly in all 27 member states without requiring separate national legislation. Any crypto company wanting to legally serve EU users must comply with MiCA — regardless of where it’s incorporated.

Does MiCA apply to crypto wallets?

It depends. If you manage your own assets through a self-custody wallet — Ledger, Trezor, Electrum — MiCA doesn’t require anything from you. If you use the integrated wallet of an exchange or centralised platform, that platform must comply with MiCA, but you as a user have no additional obligations.

Do I need a MiCA licence if I invest in cryptocurrencies?

No. Users who buy, sell, or hold cryptocurrencies for personal use don’t need any licence or authorisation. MiCA’s authorisation obligations apply exclusively to crypto service providers and certain crypto-asset issuers.

Does MiCA change crypto taxes?

No. MiCA regulates the crypto market and the companies in it — not the taxes you pay on gains. Tax rules remain governed by the legislation of each member state. Your national tax authority’s rules apply regardless of MiCA.

Does MiCA apply to stablecoins?

Yes — and with stricter rules than for other crypto-assets. Stablecoin issuers must prove they hold the real reserves backing every token, publish regular reports, and be supervised by authorities. MiCA divides stablecoins into two categories — EMTs and ARTs — each with its own compliance obligations. EMT issuers must additionally be authorised as a credit institution or electronic money institution.

What happened to crypto companies that missed the July 2026 deadline?

The 1 July 2026 deadline marked the end of all transitional arrangements. Companies that failed to obtain MiCA authorisation by that date were required to cease providing crypto-asset services in the EU or complete an orderly wind-down of their European operations.

Where can I read the full MiCA regulation?

The full text is available in Regulation (EU) 2023/1114 on markets in crypto-assets, published in the Official Journal of the European Union.

Conclusion

MiCA doesn’t change what crypto is. It changes how the companies offering crypto services in Europe operate.

The blockchain works the same way. Bitcoin remains decentralised. Ethereum too. What changes is that the exchange where you buy Bitcoin must now be authorised, keep your funds separate from its own, be transparent about costs, and have clear procedures if something goes wrong.

For the industry, MiCA represents the maturation of a sector that grew too fast without clear rules. The collapses of FTX, Celsius, and TerraUST weren’t inevitable — they were the result of an environment where companies could operate without meaningful obligations toward their users. MiCA closes that gap.

For you as a user anywhere in the EU, the direct impact is limited. You have no new obligations, no authorisation to obtain, and no change to what you owe your national tax authority. You’ll feel MiCA’s effects indirectly — through better-regulated platforms, more rigorous verification procedures at registration, and greater transparency in the services you use.

With the July 2026 deadline now passed, every crypto company serving EU users must be fully authorised or have ceased operating. The market that has emerged has fewer players than before — but those that remain are operating under a common set of rules designed to protect users across all 27 member states.

What MiCA doesn’t do: it doesn’t eliminate market volatility, it doesn’t guarantee profits, and it doesn’t change your tax obligations. Investment risk in digital assets remains real and must be evaluated carefully regardless of the regulatory environment.

As the framework matures, future iterations are already being discussed — particularly around DeFi and the gaps that MiCA’s current scope leaves unaddressed. For further reading, the full text of the regulation is available at Regulation (EU) 2023/1114 on markets in crypto-assets, and ESMA’s implementation updates can be followed at ESMA’s MiCA page.